11.12 Modelos ARCH

11.12.1 ARCH

(Engle 1982) propõe o modelo ARCH (Autoregressive Conditional Heteroscedasticity), que permite modelar a variância condicional de uma série em função dos quadrados dos retornos passados. A variância inconstante ao longo do tempo é chamada heterocedasticidade.

O modelo ARCH(\(s\)) pode ser expresso por

\[\begin{equation} y_t = a_t \tag{11.35} \end{equation}\]

\[\begin{equation} a_t = \varepsilon_t \sqrt{h_t} \tag{11.36} \end{equation}\]

\[\begin{equation} h_t = \alpha_0 + \sum_{i=1}^s \alpha_i y_{t-i}^2 \tag{11.37} \end{equation}\]

\[\begin{equation} \varepsilon_t \sim WN(0,1) \tag{11.38} \end{equation}\]

Demonstra-se que \(a_t \sim WN(0,\sigma^2_a)\), i.e., \(a_t\) tem variância constante tal que

\[\begin{equation} \sigma^2_a = \frac{\alpha_0}{1-\sum_{i=1}^s \alpha_i} \tag{11.39} \end{equation}\]

Portanto \(a_t\) possui estacionariedade fraca ou de segunda ordem. Para mais detalhes recomenda-se (Engle 1982), (Shephard 1996) e (Box et al. 2008, 413).

11.12.1.1 Clássico

Exemplo 11.54 Adaptado das documentações de tseries::garch() (Trapletti and Hornik 2024) e rugarch::ugarchspec() (Galanos 2025), simulando e ajustando um modelo ARCH\((2)\).

# libs

library(tseries)

library(rugarch)

# número de observações simuladas, 100 primeiras descartadas

n <- 1100

# coeficientes ARCH(2): alfa_0=0.1, alfa_1=0.5 e alfa_2=0.2

a <- c(0.1, 0.5, 0.2)

# \varepsilon_t, Eq. 11.38

set.seed(42); e <- rnorm(n)

# vetor para conter a série temporal yt simulada (double-precision vector)

y <- double(n)

# \sigma_a^2, Eq. 11.39

sigma2a <- sqrt(a[1]/(1-a[2]-a[3]))

# 2 primeiros valores de yt, Eq. 11.35

set.seed(314); y[1:2] <- rnorm(2, sd = sigma2a)

# gera processo ARCH(2)

for(i in 3:n){

# Eq. 11.37

ht <- a[1] + a[2]*y[i-1]^2 + a[3]*y[i-2]^2

# Eqs. 11.35 e 11.36

y[i] <- e[i]*sqrt(ht)

}

# descartando as 100 primeiras observações

y <- ts(y[101:n])

# ARCH(2)

spec <- ugarchspec(variance.model = list(garchOrder = c(2,0)),

mean.model = list(armaOrder = c(0,0)))

fit_arch <- ugarchfit(spec, y)

# diagnóstico

fit_arch##

## *---------------------------------*

## * GARCH Model Fit *

## *---------------------------------*

##

## Conditional Variance Dynamics

## -----------------------------------

## GARCH Model : sGARCH(2,0)

## Mean Model : ARFIMA(0,0,0)

## Distribution : norm

##

## Optimal Parameters

## ------------------------------------

## Estimate Std. Error t value Pr(>|t|)

## mu -0.015908 0.012160 -1.3082 0.190817

## omega 0.095962 0.009116 10.5266 0.000000

## alpha1 0.500585 0.063300 7.9082 0.000000

## alpha2 0.225688 0.049399 4.5686 0.000005

##

## Robust Standard Errors:

## Estimate Std. Error t value Pr(>|t|)

## mu -0.015908 0.011578 -1.3739 0.169473

## omega 0.095962 0.009047 10.6065 0.000000

## alpha1 0.500585 0.063524 7.8802 0.000000

## alpha2 0.225688 0.057314 3.9378 0.000082

##

## LogLikelihood : -661.2625

##

## Information Criteria

## ------------------------------------

##

## Akaike 1.3305

## Bayes 1.3502

## Shibata 1.3305

## Hannan-Quinn 1.3380

##

## Weighted Ljung-Box Test on Standardized Residuals

## ------------------------------------

## statistic p-value

## Lag[1] 0.06124 0.8045

## Lag[2*(p+q)+(p+q)-1][2] 0.16723 0.8747

## Lag[4*(p+q)+(p+q)-1][5] 1.17259 0.8195

## d.o.f=0

## H0 : No serial correlation

##

## Weighted Ljung-Box Test on Standardized Squared Residuals

## ------------------------------------

## statistic p-value

## Lag[1] 0.197 0.6571

## Lag[2*(p+q)+(p+q)-1][5] 3.104 0.3884

## Lag[4*(p+q)+(p+q)-1][9] 6.582 0.2367

## d.o.f=2

##

## Weighted ARCH LM Tests

## ------------------------------------

## Statistic Shape Scale P-Value

## ARCH Lag[3] 0.1861 0.500 2.000 0.6662

## ARCH Lag[5] 1.9632 1.440 1.667 0.4794

## ARCH Lag[7] 3.8599 2.315 1.543 0.3672

##

## Nyblom stability test

## ------------------------------------

## Joint Statistic: 0.5701

## Individual Statistics:

## mu 0.02503

## omega 0.35415

## alpha1 0.25326

## alpha2 0.21252

##

## Asymptotic Critical Values (10% 5% 1%)

## Joint Statistic: 1.07 1.24 1.6

## Individual Statistic: 0.35 0.47 0.75

##

## Sign Bias Test

## ------------------------------------

## t-value prob sig

## Sign Bias 1.1810 0.2379

## Negative Sign Bias 0.9791 0.3278

## Positive Sign Bias 0.3806 0.7035

## Joint Effect 1.5812 0.6637

##

##

## Adjusted Pearson Goodness-of-Fit Test:

## ------------------------------------

## group statistic p-value(g-1)

## 1 20 16.00 0.6573

## 2 30 30.98 0.3664

## 3 40 37.68 0.5300

## 4 50 47.80 0.5218

##

##

## Elapsed time : 0.08645487# previsão 20 períodos à frente

fcast <- ugarchforecast(fit_arch, n.ahead = 20)

plot(fcast, which = 1) # 1 = Conditional mean forecast

11.12.2 GARCH

(Bollerslev 1986) estendeu o trabalho original de Engle, propondo o modelo GARCH (Generalized Autoregressive Conditional Heteroscedasticity), que permite que a variância condicional não dependa somente dos quadrados dos retornos passados, mas também da própria variância passada. O modelo GARCH\((r,s)\) é definido pelas Eq. (11.35), (11.36) e (11.38), com \(h_t\) dado pela Eq. (11.40).

\[\begin{equation} h_t = \alpha_0 + \sum_{i=1}^s \alpha_i y_{t-i}^2 + \sum_{i=1}^r \beta_i h_{t-i} \tag{11.40} \end{equation}\]

Para esta formulação \(a_t\) também possui variância constante, definida pela Eq. (11.41).

\[\begin{equation} \sigma^2_a = \frac{\alpha_0}{1-\sum_{i=1}^s \alpha_i - \sum_{i=1}^r \beta_i} \tag{11.41} \end{equation}\]

11.12.2.1 Clássico

Exemplo 11.55 Adaptado da documentação de tseries::garch(), simulando e ajustando um modelo GARCH(1,1). Lembre-se que “[t]he [a]utocovariances [d]o [n]ot [a]lways [d]ecrease” (Francq and Zakoian 2010, 51).

# libs

library(tseries)

library(rugarch)

# número de observações simuladas, 100 primeiras descartadas

n <- 1100

# coeficientes ARCH(1): alfa_0=0.1 e alfa_1=0.5

a <- c(0.1, 0.5)

# coeficiente GARCH(s,1): beta_1=0.3

b <- c(0.3)

# \varepsilon_t, Eq. 11.38

set.seed(42); e <- rnorm(n)

# vetor para conter a série temporal yt simulada (double-precision vector)

y <- double(n)

# vetor para conter a série temporal de ht

h <- double(n)

# Eqs. 11.34 e 11.40

set.seed(314); y[1] <- rnorm(1, sd = sqrt(a[1]/(1-a[2]-b[1])))

# gera processo GARCH(1,1)

for(i in 2:n){

# Eq. 11.39

h[i] <- a[1] + a[2]*y[i-1]^2 + b[1]*h[i-1]

# Eqs. 11.34 e 11.35

y[i] <- e[i]*sqrt(h[i])

}

# descartando as 100 primeiras observações

y <- ts(y[101:n])

# GARCH(1,1)

spec <- ugarchspec(variance.model = list(garchOrder = c(1,1)),

mean.model = list(armaOrder = c(0,0)))

fit_garch <- ugarchfit(spec, y)

# diagnóstico

fit_garch##

## *---------------------------------*

## * GARCH Model Fit *

## *---------------------------------*

##

## Conditional Variance Dynamics

## -----------------------------------

## GARCH Model : sGARCH(1,1)

## Mean Model : ARFIMA(0,0,0)

## Distribution : norm

##

## Optimal Parameters

## ------------------------------------

## Estimate Std. Error t value Pr(>|t|)

## mu -0.018259 0.014908 -1.2248 0.22064

## omega 0.073548 0.014315 5.1377 0.00000

## alpha1 0.468977 0.061610 7.6121 0.00000

## beta1 0.397669 0.061347 6.4823 0.00000

##

## Robust Standard Errors:

## Estimate Std. Error t value Pr(>|t|)

## mu -0.018259 0.014069 -1.2978 0.194346

## omega 0.073548 0.017321 4.2462 0.000022

## alpha1 0.468977 0.070549 6.6475 0.000000

## beta1 0.397669 0.084187 4.7236 0.000002

##

## LogLikelihood : -866.4694

##

## Information Criteria

## ------------------------------------

##

## Akaike 1.7409

## Bayes 1.7606

## Shibata 1.7409

## Hannan-Quinn 1.7484

##

## Weighted Ljung-Box Test on Standardized Residuals

## ------------------------------------

## statistic p-value

## Lag[1] 0.05405 0.8162

## Lag[2*(p+q)+(p+q)-1][2] 0.17145 0.8721

## Lag[4*(p+q)+(p+q)-1][5] 1.21927 0.8084

## d.o.f=0

## H0 : No serial correlation

##

## Weighted Ljung-Box Test on Standardized Squared Residuals

## ------------------------------------

## statistic p-value

## Lag[1] 0.872 0.3504

## Lag[2*(p+q)+(p+q)-1][5] 4.705 0.1783

## Lag[4*(p+q)+(p+q)-1][9] 7.756 0.1437

## d.o.f=2

##

## Weighted ARCH LM Tests

## ------------------------------------

## Statistic Shape Scale P-Value

## ARCH Lag[3] 0.000114 0.500 2.000 0.9915

## ARCH Lag[5] 3.394667 1.440 1.667 0.2374

## ARCH Lag[7] 4.871646 2.315 1.543 0.2378

##

## Nyblom stability test

## ------------------------------------

## Joint Statistic: 0.4709

## Individual Statistics:

## mu 0.02895

## omega 0.22996

## alpha1 0.30454

## beta1 0.28856

##

## Asymptotic Critical Values (10% 5% 1%)

## Joint Statistic: 1.07 1.24 1.6

## Individual Statistic: 0.35 0.47 0.75

##

## Sign Bias Test

## ------------------------------------

## t-value prob sig

## Sign Bias 1.5441 0.1229

## Negative Sign Bias 1.0226 0.3067

## Positive Sign Bias 0.7825 0.4341

## Joint Effect 2.4511 0.4842

##

##

## Adjusted Pearson Goodness-of-Fit Test:

## ------------------------------------

## group statistic p-value(g-1)

## 1 20 18.20 0.5091

## 2 30 25.88 0.6319

## 3 40 45.84 0.2096

## 4 50 54.80 0.2640

##

##

## Elapsed time : 0.04700303# previsão 20 períodos à frente

fcast <- ugarchforecast(fit_garch, n.ahead = 20)

plot(fcast, which = 1) # 1 = Conditional mean forecast

11.12.2.2 Bayesiano

A função bayesforecast::garch() (Matamoros and Torres 2020) implementa um modelo GARCH\((s,k,h)\) baseado em (Ardia and Hoogerheide 2010) e (Fonseca et al. 2019). As três componentes \((s,k,h) \equiv (s,r,h)\) são a ordem do ARCH (\(s\)), a ordem do GARCH (\(k \equiv r\)) e a ordem do MGARCH (\(h\)) (Bollerslev et al. 1988). Segundo a documentação, as prioris padrão utilizadas no modelo MGARCH são:

- ar ~ normal(0,0.5)

- ma ~ normal(0,0.5)

- mu0 ~ t-student(0,2.5,6)

- sigma0 ~ t-student(0,1,7)

- arch ~ normal(0,0.5)

- garch ~ normal(0,0.5)

- mgarch ~ normal(0,0.5)

- dfv ~ gamma(2,0.1)

- breg ~ t-student(0,2.5,6)

Para mais detalhes veja (Engle Robert and Kevin 2001) e (Engle 2002).

Exemplo 11.56 Considere a série \(y_t\) gerada no Exemplo 11.55.

# libs

library(bayesforecast)

# GARCH(1,1)

fit_garch_bayes <- bayesforecast::garch(y, order = c(1,1,0))

fit_garch_varstan <- bayesforecast::varstan(fit_garch_bayes, iter = 500,

chains = 1, quiet = TRUE)##

## SAMPLING FOR MODEL 'tgarch' NOW (CHAIN 1).

## Chain 1:

## Chain 1: Gradient evaluation took 0.002354 seconds

## Chain 1: 1000 transitions using 10 leapfrog steps per transition would take 23.54 seconds.

## Chain 1: Adjust your expectations accordingly!

## Chain 1:

## Chain 1:

## Chain 1: Iteration: 1 / 500 [ 0%] (Warmup)

## Chain 1: Iteration: 50 / 500 [ 10%] (Warmup)

## Chain 1: Iteration: 100 / 500 [ 20%] (Warmup)

## Chain 1: Iteration: 150 / 500 [ 30%] (Warmup)

## Chain 1: Iteration: 200 / 500 [ 40%] (Warmup)

## Chain 1: Iteration: 250 / 500 [ 50%] (Warmup)

## Chain 1: Iteration: 251 / 500 [ 50%] (Sampling)

## Chain 1: Iteration: 300 / 500 [ 60%] (Sampling)

## Chain 1: Iteration: 350 / 500 [ 70%] (Sampling)

## Chain 1: Iteration: 400 / 500 [ 80%] (Sampling)

## Chain 1: Iteration: 450 / 500 [ 90%] (Sampling)

## Chain 1: Iteration: 500 / 500 [100%] (Sampling)

## Chain 1:

## Chain 1: Elapsed Time: 0.616 seconds (Warm-up)

## Chain 1: 0.358 seconds (Sampling)

## Chain 1: 0.974 seconds (Total)

## Chain 1:## mean se 5% 95% ess Rhat

## mu0 -0.0145 0.0009 -0.0383 0.0099 265.6395 0.9996

## sigma0 0.0828 0.0010 0.0583 0.1106 283.0997 0.9983

## arch 0.4844 0.0036 0.4055 0.5701 234.7433 1.0200

## garch 0.3662 0.0036 0.2781 0.4588 181.7439 1.0094

## loglik -869.9343 0.0964 -873.0877 -868.2888 273.2528 0.9986

#### Diagnóstico

#### Diagnóstico

Ao ajustar um modelo bayesiano usando bayesforecast (que usa internamente Stan), o resumo do objeto ajustado inclui estatísticas de diagnóstico para cada parâmetro estimado. Dois dos principais são ess e Rhat.

ess: Effective Sample Size

Definição: O tamanho efetivo da amostra (ESS) mede quanta informação independente suas cadeias MCMC contêm para um parâmetro.

Intuição: Mesmo que você extraia, digamos, 2000 amostras de cada cadeia, as amostras são autocorrelacionadas (não independentes). O ESS informa a quantas amostras independentes suas cadeias são efetivamente equivalentes.

Interpretação: - ESS mais alto → estimativas posterioris mais confiáveis. - Como regra geral: - ESS > 1000 por parâmetro → bom. - ESS < 100 → indica forte autocorrelação; considere executar cadeias mais longas ou melhorar a amostragem.

bayesforecast relata ambos:

- ess_bulk: para a parte central (volume) da posteriori.

- ess_tail: para as caudas (valores extremos) da posteriori.

—

11.12.2.2.1 Rhat: Fator Potencial de Redução de Escala

Definição:

Rhat compara a variância entre cadeias com a variância dentro da cadeia para cada parâmetro. É conhecido como estatística de Gelman-Rubin.

Intuição:

Se múltiplas cadeias se misturaram bem e convergiram para o mesmo posterior, suas variâncias devem ser semelhantes → Rhat ≈ 1.

Interpretação:

- Rhat ≈ 1.00 → boa convergência.

- Rhat > 1.00 → possível não convergência, indicam que você deve executar novamente ou reespecificar o modelo.

—

Exercício 11.32

- No Exemplo 11.54 verifique a equivalência entre os modelos ARCH\((2)\), GARCH\((0,2)\) de

tseriese GARCH\((2,0,0)\) debayesforecast. - Veja https://asael697.r-universe.dev/bayesforecast.

- Veja https://cran.r-universe.dev/bayesforecast/doc/manual.html.

- Veja http://fmwww.bc.edu/EC-C/S2014/823/EC823.S2014.nn09.slides.pdf.

11.12.3 IGARCH

Engle and Bollerslev (1986) propõem o modelo IGARCH, “uma nova classe de modelos definidos para serem integrados em variância” a partir da restrição \(\sum_{i=1}^{s} \alpha_i + \sum_{i=1}^{r} \beta_i = 1\) na Eq. (11.40).

11.12.4 EGARCH

Nelson (1991) propõe o modelo EGARCH com o objetivo de “acomodar a relação assimétrica entre os retornos das ações e as mudanças na volatilidade”. Seguindo a notação de Vrontos et al. (2000),

\[\begin{equation} \log h_t = \alpha_0 + \sum_{i=1}^s \theta_i a_{t-i} + \gamma_i (|a_{t-i}|-E|a_{t-i}|) + \sum_{i=1}^r \beta_i h_{t-i} \tag{11.42} \end{equation}\]

\[\begin{equation} E|a_{t-i}| = \frac{\Gamma(\frac{2}{\nu})}{[\Gamma(\frac{1}{\nu}) \Gamma(\frac{3}{\nu})]^{1/2}} \tag{11.43} \end{equation}\]

11.12.5 ARMA-GARCH

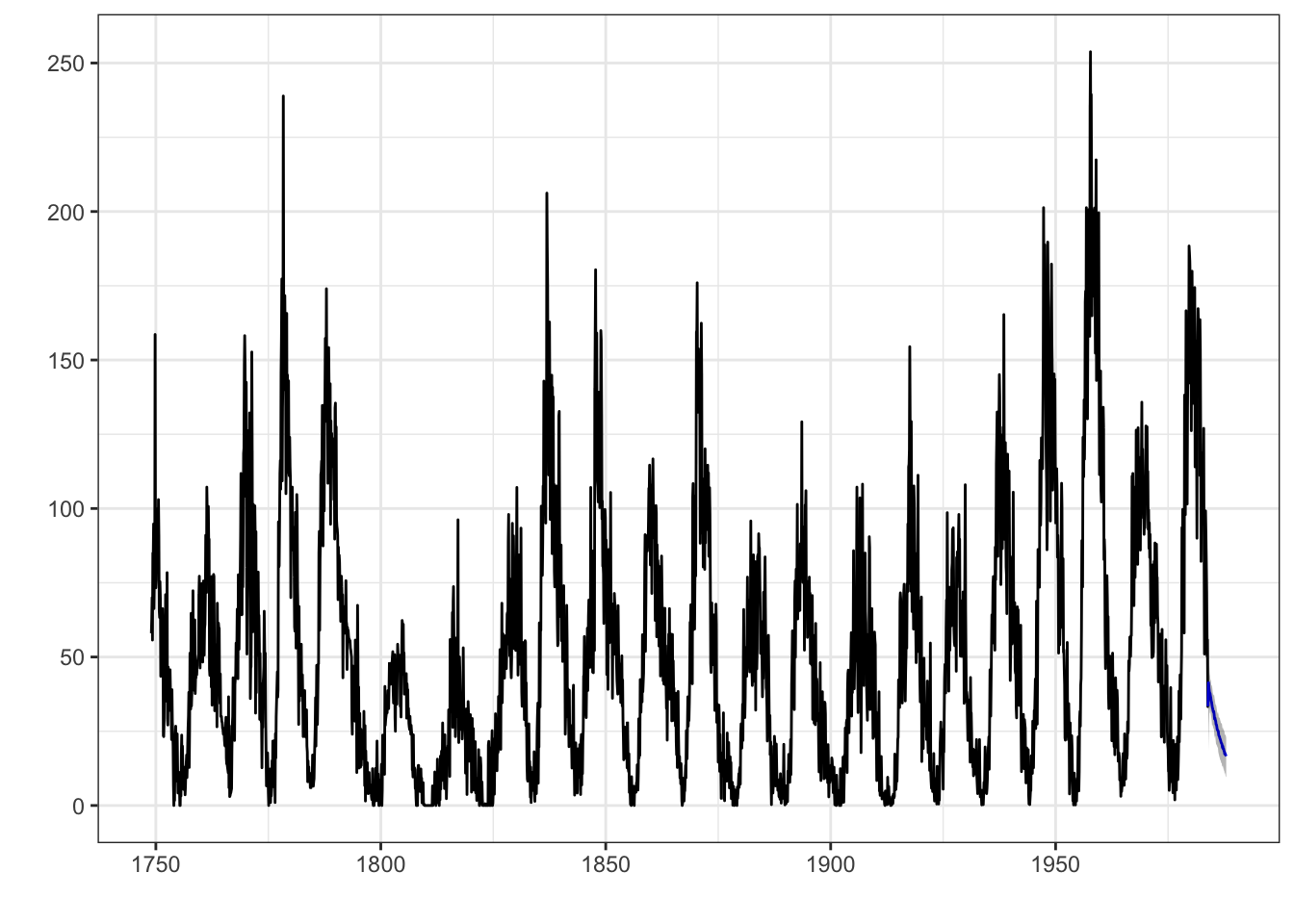

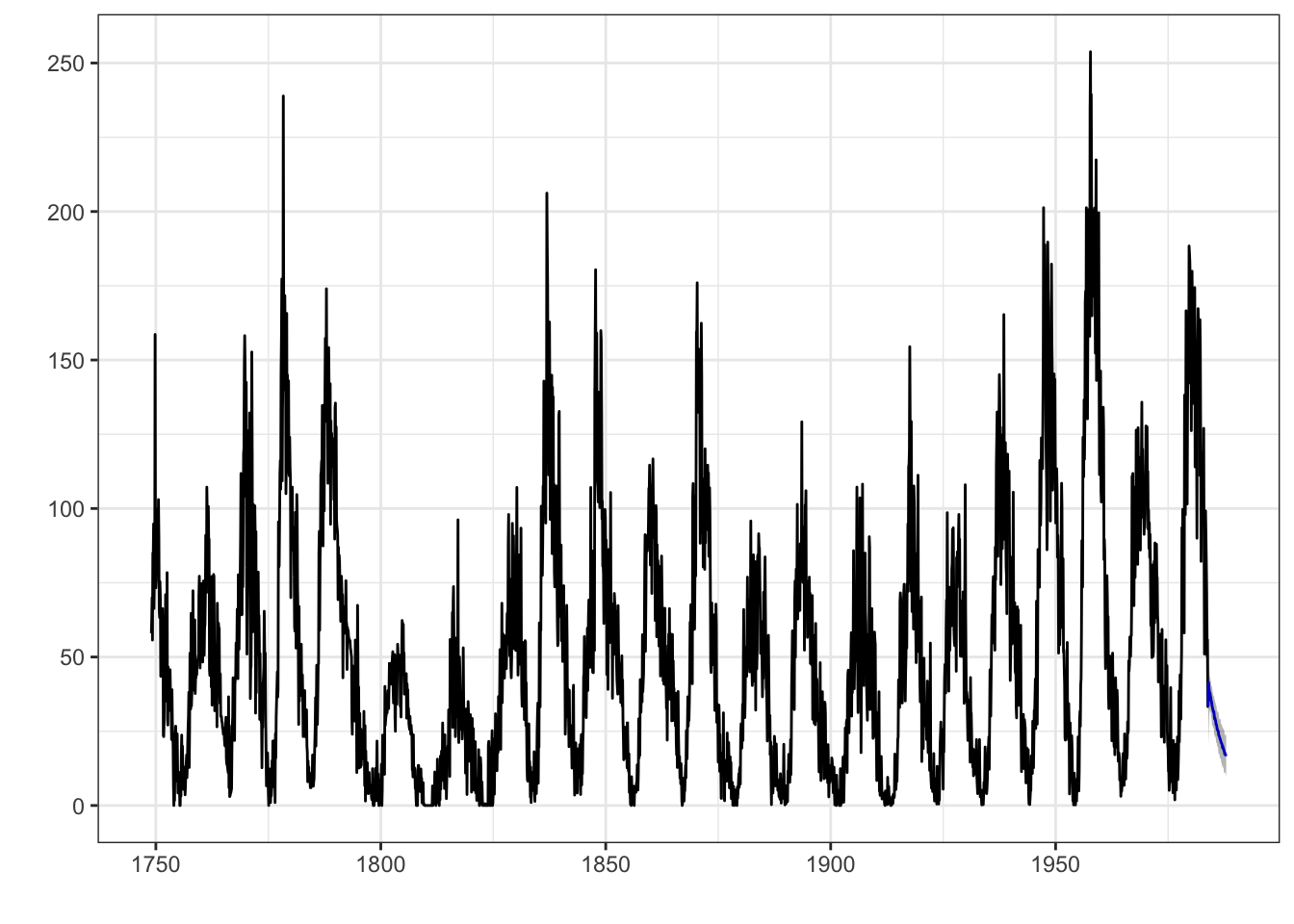

Exemplo 11.57 Considere a série temporal r unlist(tsdl::meta_tsdl[20,2][[1]][[1]]) apresentada por r tsdl::meta_tsdl[20,1], disponível em tsdl::tsdl[[20]]22.

library(forecast)

library(bayesforecast)

# ajustando um modelo ARIMA automático

y <- tsdl::tsdl[[20]]

# ARIMA(2,1,2)

forecast::auto.arima(y)## Series: y

## ARIMA(2,1,2)

##

## Coefficients:

## ar1 ar2 ma1 ma2

## 1.3467 -0.3963 -1.7710 0.8103

## s.e. 0.0303 0.0287 0.0205 0.0194

##

## sigma^2 = 243.8: log likelihood = -11745.5

## AIC=23500.99 AICc=23501.01 BIC=23530.71# ajustando ARMA(2,2)-GARCH(1,1) para a série com uma diferença via bayesforecast

fit_garch_bayes <- bayesforecast::garch(y, order = c(1,1,0), arma = c(2,2))

fit_garch_varstan <- bayesforecast::varstan(fit_garch_bayes, iter = 500, chains = 1)##

## SAMPLING FOR MODEL 'tgarch' NOW (CHAIN 1).

## Chain 1: Rejecting initial value:

## Chain 1: Log probability evaluates to log(0), i.e. negative infinity.

## Chain 1: Stan can't start sampling from this initial value.

## Chain 1:

## Chain 1: Gradient evaluation took 0.008172 seconds

## Chain 1: 1000 transitions using 10 leapfrog steps per transition would take 81.72 seconds.

## Chain 1: Adjust your expectations accordingly!

## Chain 1:

## Chain 1:

## Chain 1: Iteration: 1 / 500 [ 0%] (Warmup)

## Chain 1: Iteration: 50 / 500 [ 10%] (Warmup)

## Chain 1: Iteration: 100 / 500 [ 20%] (Warmup)

## Chain 1: Iteration: 150 / 500 [ 30%] (Warmup)

## Chain 1: Iteration: 200 / 500 [ 40%] (Warmup)

## Chain 1: Iteration: 250 / 500 [ 50%] (Warmup)

## Chain 1: Iteration: 251 / 500 [ 50%] (Sampling)

## Chain 1: Iteration: 300 / 500 [ 60%] (Sampling)

## Chain 1: Iteration: 350 / 500 [ 70%] (Sampling)

## Chain 1: Iteration: 400 / 500 [ 80%] (Sampling)

## Chain 1: Iteration: 450 / 500 [ 90%] (Sampling)

## Chain 1: Iteration: 500 / 500 [100%] (Sampling)

## Chain 1:

## Chain 1: Elapsed Time: 27.039 seconds (Warm-up)

## Chain 1: 33.128 seconds (Sampling)

## Chain 1: 60.167 seconds (Total)

## Chain 1:

# # tomando uma diferença da série

# ydiff <- diff(y)

# fit_garch_bayes_diff <- bayesforecast::garch(ydiff, order = c(1,1,0), arma = c(2,2)) # ajusta ARMA(2,2)-GARCH(1,1)

# fit_garch_varstan_diff <- bayesforecast::varstan(fit_garch_bayes_diff, iter = 500, chains = 1)

# check_residuals(fit_garch_varstan_diff) # análise de resíduos

# bf <- bayesforecast::forecast(fit_garch_varstan_diff, h = 48)

# # desfazendo as diferenças

# bf$x <- diffinv(bf$x, xi = y[1])

# bf$mean <- diffinv(bf$mean, xi = y[length(y)])

# autoplot(bf) # projetando 48 passosA função rugarch::ugarchspec() (Galanos 2025) permite ajustar um modelo ARFIMA-GARCH, com variantes do modelo GARCH e variáveis externas (veja documentação).

# libs

library(forecast)

library(rugarch)

# ajustando um modelo ARIMA automático

y <- tsdl::tsdl[[37]]

# ARIMA(1,1,1)

(fit_arima <- forecast::auto.arima(y))## Series: y

## ARIMA(1,1,1)

##

## Coefficients:

## ar1 ma1

## -0.5322 0.9476

## s.e. 0.1389 0.0657

##

## sigma^2 = 95.43: log likelihood = -199.28

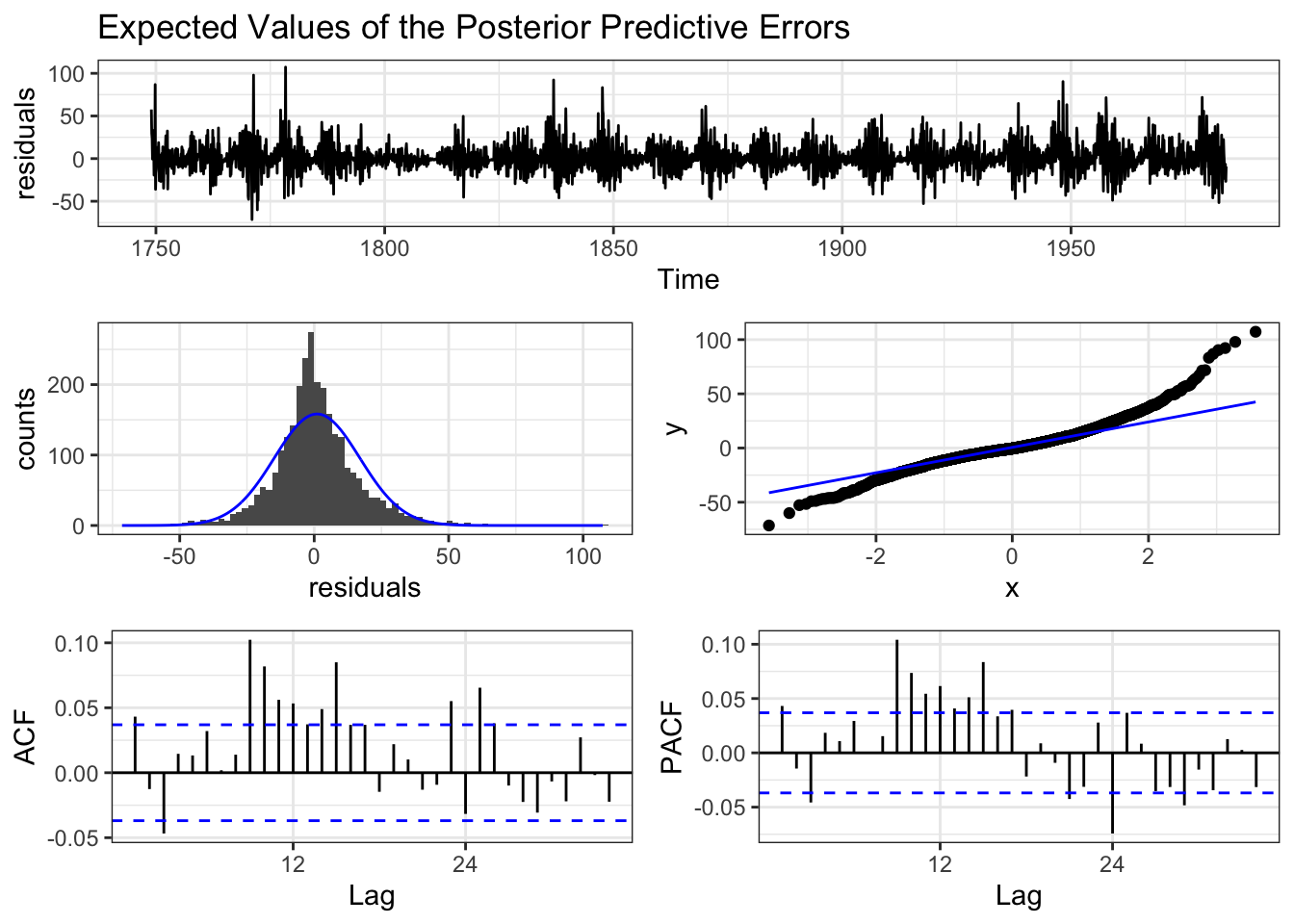

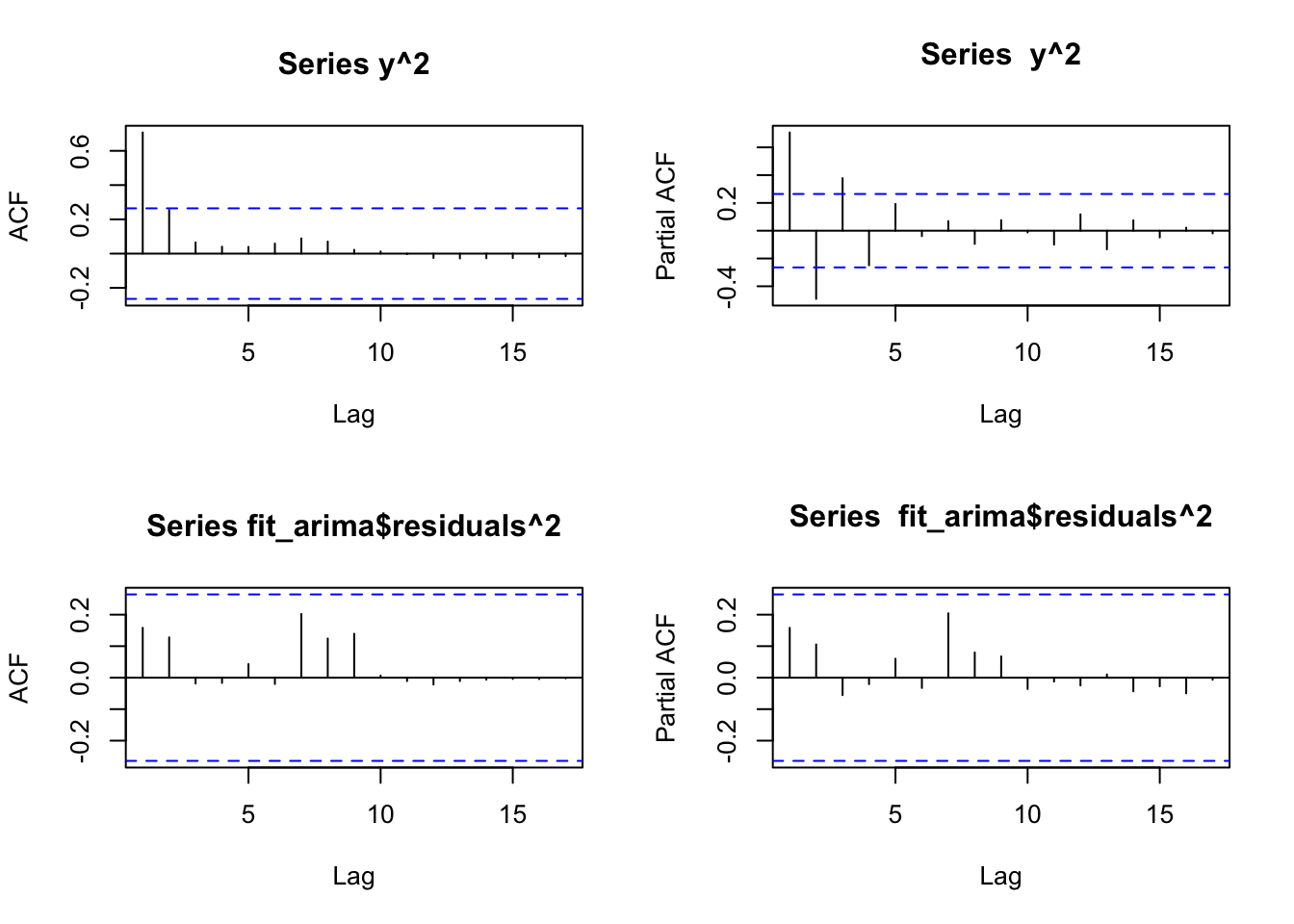

## AIC=404.57 AICc=405.05 BIC=410.54# avaliando a série ao quadrado e os resíduos ao quadrado do ARIMA(1,1,1)

par(mfrow=c(2,2))

acf(y^2)

pacf(y^2)

acf(fit_arima$residuals^2)

pacf(fit_arima$residuals^2)

# tomando uma diferença da série

ydiff <- diff(y)

# ajustando ARMA-GARCH para a série com uma diferença via rugarch

spec <- ugarchspec(

mean.model = list(armaOrder = c(2,2), arfima = FALSE),

variance.model = list(garchOrder = c(0,1))

)

fit_garch <- ugarchfit(spec = spec, data = y, solver.control = list(trace=0))

fit_garch##

## *---------------------------------*

## * GARCH Model Fit *

## *---------------------------------*

##

## Conditional Variance Dynamics

## -----------------------------------

## GARCH Model : sGARCH(0,1)

## Mean Model : ARFIMA(2,0,2)

## Distribution : norm

##

## Optimal Parameters

## ------------------------------------

## Estimate Std. Error t value Pr(>|t|)

## mu 9.766928 0.729527 13.38803 0.00000

## ar1 0.973898 0.396542 2.45598 0.01405

## ar2 0.315426 0.525520 0.60022 0.54836

## ma1 -0.033163 0.048437 -0.68466 0.49356

## ma2 -1.091586 0.082845 -13.17617 0.00000

## omega 0.744128 5.858005 0.12703 0.89892

## beta1 0.999000 0.082035 12.17775 0.00000

##

## Robust Standard Errors:

## Estimate Std. Error t value Pr(>|t|)

## mu 9.766928 1.68982 5.779859 0.000000

## ar1 0.973898 1.37428 0.708662 0.478534

## ar2 0.315426 1.83710 0.171698 0.863675

## ma1 -0.033163 0.15565 -0.213058 0.831282

## ma2 -1.091586 0.29994 -3.639348 0.000273

## omega 0.744128 23.03233 0.032308 0.974226

## beta1 0.999000 0.32684 3.056497 0.002239

##

## LogLikelihood : -190.7872

##

## Information Criteria

## ------------------------------------

##

## Akaike 7.1923

## Bayes 7.4477

## Shibata 7.1645

## Hannan-Quinn 7.2911

##

## Weighted Ljung-Box Test on Standardized Residuals

## ------------------------------------

## statistic p-value

## Lag[1] 0.5043 0.4776

## Lag[2*(p+q)+(p+q)-1][11] 4.4613 0.9972

## Lag[4*(p+q)+(p+q)-1][19] 8.3803 0.7387

## d.o.f=4

## H0 : No serial correlation

##

## Weighted Ljung-Box Test on Standardized Squared Residuals

## ------------------------------------

## statistic p-value

## Lag[1] 6.099 0.01352

## Lag[2*(p+q)+(p+q)-1][2] 7.204 0.01052

## Lag[4*(p+q)+(p+q)-1][5] 9.123 0.01541

## d.o.f=1

##

## Weighted ARCH LM Tests

## ------------------------------------

## Statistic Shape Scale P-Value

## ARCH Lag[2] 2.055 0.500 2.000 0.1517

## ARCH Lag[4] 3.418 1.397 1.611 0.2100

## ARCH Lag[6] 3.772 2.222 1.500 0.3403

##

## Nyblom stability test

## ------------------------------------

## Joint Statistic: 13.3381

## Individual Statistics:

## mu 0.03699

## ar1 0.03213

## ar2 0.03140

## ma1 0.03472

## ma2 0.06054

## omega 0.58634

## beta1 0.46952

##

## Asymptotic Critical Values (10% 5% 1%)

## Joint Statistic: 1.69 1.9 2.35

## Individual Statistic: 0.35 0.47 0.75

##

## Sign Bias Test

## ------------------------------------

## t-value prob sig

## Sign Bias 0.06203 0.950788

## Negative Sign Bias 3.02330 0.003938 ***

## Positive Sign Bias 1.64256 0.106749

## Joint Effect 14.34114 0.002476 ***

##

##

## Adjusted Pearson Goodness-of-Fit Test:

## ------------------------------------

## group statistic p-value(g-1)

## 1 20 17.36 0.5652

## 2 30 25.18 0.6688

## 3 40 30.09 0.8463

## 4 50 44.09 0.6720

##

##

## Elapsed time : 0.167192# previsão com o modelo

fcast <- ugarchforecast(fit_garch)

# plot(fcast, ask = FALSE)

# desfazendo a diferença

# fcast2 <- fcast

# fcast2@model$modeldata$data <- as.matrix(diffinv(fcast2@model$modeldata$data, xi = y[1]))

# fcast2@model$modeldata$data <- y[-1]

# fcast2@forecast$seriesFor <- as.matrix(diffinv(fcast2@forecast$seriesFor)[-1])

# plot(fcast2)